The Strengthening of the Dollar and the Upcoming US Elections Mean Tough Times for Mexico

This article is an excerpt from UFM Market Trends’ report on the second quarter of the Mexican economy.

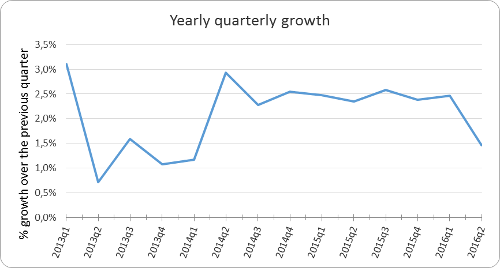

Mexico’s GDP growth remains in its expected growth range. The country’s economy is projected to grow 2.6% by the end of the year.

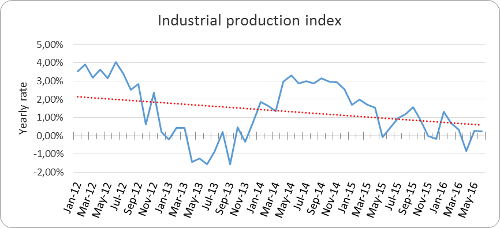

Industrial activity fails to pick up. Manufacturing, construction, and mining are basically paralyzed. The industrial sector is one of the most important for the Mexican economy and its inactivity is not helping Mexico grow at higher rates.

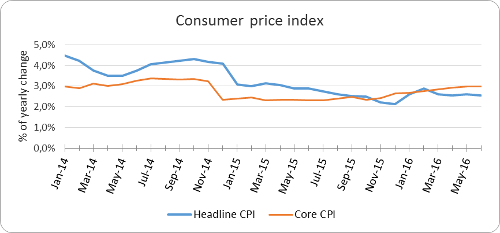

Last year, Mexico closed with historically low inflation rates. However, this has changed throughout 2016. Core inflation, which excludes goods with very volatile prices, has been greater than general inflation since November 2015. Prices are also rising due to the depreciation of the peso. This evolution of inflation prices should be paid close attention to in the coming months.

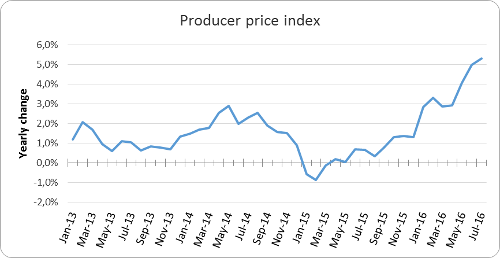

Another measure affecting the industrial sector is the Producer Price Index, which does not bring good news for industries. Since early 2016, producer prices have been growing at increasing rates. High production costs create another obstacle for the struggling industrial sector.

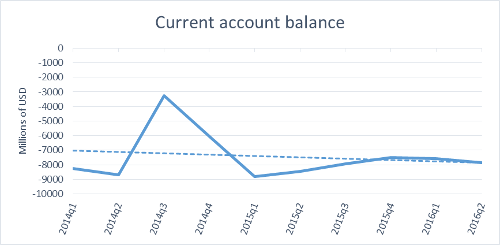

Low oil prices, the deteriorating competitiveness of Pemex, and the dormant industrial sector are factors that do not help reverse Mexico’s trade deficit. Another quarter has gone by and Mexico’s trade balances still has a negative trend. Exports opened this year with poor growth rates and have not improved over the second quarter of the year.

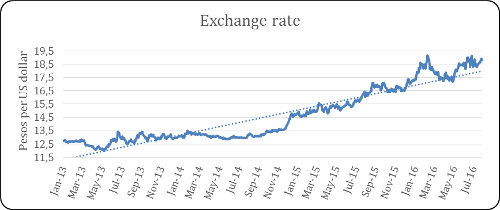

The Mexican peso suffers is suffering due to the country’s trade deficit, largely explaining the currency’s depreciation that has taken place since mid-2014. Another factor generating uncertainty is the outcome of the upcoming US elections. The short positions taken by investors against the peso come from this speculation created by the US elections. At the same time, the expectation that the Fed will raise interest rates once more puts more pressure to take short positions against the peso. These factors have merges and have been a headache for Mexico’s central bank, which has had to raise interest rates in February and July to protect the peso. The Mexican peso is one of the most liquid currencies out there, making it sensitive to speculative decisions.

More details about Mexico´s economy can be seen in the quarterly report Market Trends.

Get our free exclusive report on our unique methodology to predict recessions

Edgar Ortiz

Edgar Ortiz has a degree in Law from the Francisco Marroquín University. He holds a master in Austrian Economics at the Rey Juan Carlos University in Madrid. He is the executive director of the Center of Economic and Social Studies (CEES). He is a professor of economics at the Francisco Marroquín University, and he is also an analyst on issues related to the situation at Canal Antigua. He works as an associate lawyer at Estudio Jurídico Rivera.

Get our free exclusive report on our unique methodology to predict recessions