Nobel Prize in Economics 2022: A Guide for Dummies

The 2022 Nobel Prize in Economics has been awarded to Ben Bernanke, Douglas Diamond and Philip Dybvig. These authors won the highest award in the economic discipline for their contributions on the role of the banking sector in the economy and in particular its role during financial crises.

In this article, I will analyze the Diamond-Dybvig model, which is the main reason why the Nobel Prize was awarded to Douglas Diamond and Philip Dybvig.

Both Diamond and Dybvig were already well-known and often cited for the model that bears their names, a model explained in detail in an academic article published in 1983. It will be precisely this academic paper that we will break down in this article. In a future article, I will criticize the Diamond-Dybvig model.

The Diamond-Dybvig Model: A “Competitive” Result

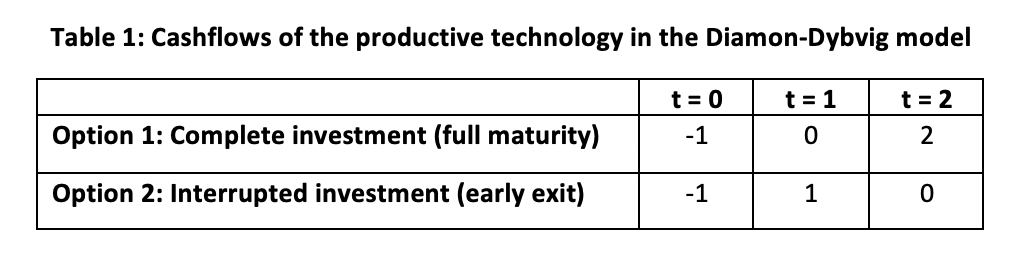

In their model, Diamond and Dybvig describe an economy at three moments in time, t=0, t=1 and t=2. There is one single good in the model that is produced and consumed. Every person receives one unit of that good at time t=0. When it comes to production, there is a single productive technology, which can be used by everyone. This productive technology requires a unit of investment at time t=1 and allows one unit of the good to be produced at time t=1 or 2 units of the good at time t=2. Since there exists only one good in this hypothetical economy, both the investment itself and the return on investment occur in terms of exactly the same good[1] .

In sum, the diagram of productive technology in the Diamond-Dybvig model is as follows:

Source: based on Diamond-Dybvig (1983). In the original model, option 1 matures with yield R>1.

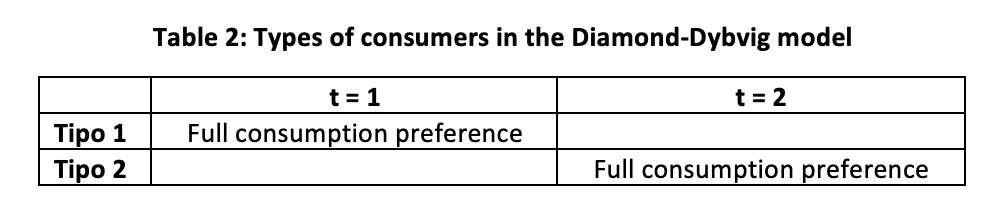

Once the productive technology is presented, we are told that consumers can be of two types: type 1 consumers that want to consume the only good available in period 1 and type 2 consumers that only want to consume in period 2.

A peculiarity of the model is that, at time t=0, consumers are still unaware of what type of consumer they are. That is, in the initial period, consumers have no idea whether they will want to consume at t=1 or at t=2. Consumers find out what type of consumer they are in period t=1. This assumption is simply unwarranted (besides some other earlier mentioned assumptions), but I will save my criticism for later.

Therefore, our scheme of the two consumer types in the Diamond-Dybvig model looks like this:

Source: based on Diamond-Dybvig (1983)

If, in this scheme, a consumer knew that he was going to be a type 1 consumer, he could save the goods of the initial period and only type 2 consumers would invest. But since risk is not taken into account and, in addition, there is uncertainty about what type of consumer each person will be, then it is logical that at time t=0 all initial goods are fully invested by everyone.

At the start of t=1, consumers will already know whether they are type 1 or type 2. At this point, they could exchange, if they wanted, the output available at t=1 and t=2. However, exchange makes no sense at all according to these assumptions. At t=1, everyone simply consumes what they produce[2] .

At t=1, if a consumer discovers that he is a type 1 consumer, he will stop being a producer and become a consumer for all the goods available to him: type 1 consumers always interrupt the production process and will never continue to produce in t=2 (type 1 consumers find no utility in consuming at t=2, even though they might have more goods available at that moment). Similarly, at t=1, if a consumer discovers that he is a type 2 consumer, he will not consume anything at t=1 and will continue to produce until the end, when he obtains two units at t=2. Type 2 consumers never interrupt the production process (consumption at t=1 does not have any utility for type 2 consumers).

This scheme is what the model sets forth as a “competitive” scheme. Curiously, the term “competitive” is often used by economists to refer to an unhampered market, without any regulation or intervention. Of course, the entire scheme that we just expounded has absolutely nothing to do with an unregulated market, but again, I will leave any criticism for later.

The Diamond-Dybvig Model: Establishing “Optimal” Insurance Contracts

We economists love to intervene in markets, so after seeing the alleged problems of a competitive market, that is, of a market without intervention, the authors propose a possibility of establishing an optimum; this optimum is almost always based on some type of criteria established, most of the time quite arbitrarily, by the researcher himself.

In the Diamond-Dybvig model, the latest Nobel Prize winners propose an optimal insurance contract. Let us examine what they mean by this.

The model assumes that type 2 consumers have higher utility than type 1 consumers[3] . The model further assumes that consumers are naturally risk-averse[4]. Being risk-averse, in the Diamond-Dybvig model, means that, since it is not known in advance, at t=0, whether a consumer will be a type 1 consumer or a type 2 consumer, expected consumption is greater than 1 at t=1 and less than 2 at t=2 (this is a kind of hedge against being a type 1 consumer with little utility). Therefore, if some type of insurance contract could be established that would hedge against becoming a type 1 consumer by paying something only in case of being a type 2 consumer, it would be established. This is what Diamond and Dybvig call an optimal insurance contract that improves the competitive situation.

The Banking Sector Makes Its Entrance

It is at this point that the Nobel Prize winners finally introduce the banking sector to their model. Banks can provide the type of insurance that consumers need in the event of becoming a type 1 consumer and they do so through demand deposit contracts.

The bank pays interest on deposits while providing liquidity to consumers. In this case, liquidity is defined as the possibility of becoming consumers before reaching t=2. If consumers become a consumer type 1, they receive the interest rate r1 (which is greater than 1; if they become consumers in at t=2, they receive the interest rate r2 (which is less than 2).

The bank then performs the function of insurance. Specifically, the bank splits the profits of the most productive method of production that yields a return of 2 between r1 and r2. That is, the bank acts as hedge and redistributes the income from the higher productivity of waiting until t=2 between those who are unlucky enough to become type 1 consumers and those who are lucky enough to become type 2 consumers. Type 2 consumers could be said to pay a premium and type 1 consumers earn a premium.

Here I am disregarding some details such as the ownership of the bank (assumed to be a “community-owned” bank), the need for the bank to be liquidated at the end of period 2 (these issues will be touched upon in my criticism). Nor is it necessary or crucial to explain the specific payment received by type 1 consumers (r1) and the specific payment made by type 2 consumers (r2).

Well, now that we have seen what the function of banking is in the Diamond-Dybvig model, let us now examine how financial panics in the form of bank runs can be introduced into this model.

Nash Equilibria in the Diamond-Dybvig Model

Now that we have our model practically complete, the authors propose their idea of possible Nash equilibria in our particular economy. By Nash equilibria we basically mean rest points in the economy, even if those points are inefficient.

There are two possible equilibria in the Diamond-Dybvig model: one efficient and one inefficient. Let us start with the efficient equilibrium.

The efficient equilibrium occurs when in period t=1 all type 1 consumers turn their deposits into cash and become consumers. Within the parameters of the model, they will do it in a favorable manner for them compared to the supposed competitive situation, since now they not only receive the same amount invested, but also interest or a positive return on investment that, as we have previously commented, is equal to r1. In this equilibrium, all type 2 consumers expect investments to provide a positive return and receive r2. Let us recall that r2 is less than 2, but type 2 consumers are also happy with this result, since they protected themselves against the eventuality of becoming type 1 consumers, that is, the difference between what they receive from the bank in the form of r2 and the total investment return equals the insurance payment, a payment that is transferred to and received by type 1 consumers.

There is another possible equilibrium, but this time it is an inefficient equilibrium. The inefficient equilibrium even worsens the supposedly competitive position.

In the inefficient equilibrium, when t=1 arrives, all consumers panic and try to withdraw their bank deposits. This occurs because the value of the deposits is greater than the liquidation value of all assets. Recall that the bank has promised to deliver a positive return on deposits (r1), while the assets at t=1 have not matured yet, which means that de facto, if they want to sell them, they cannot give a positive return to everyone. The bank could sell all the assets and return the deposits in full but pay absolutely no interest. It must be remembered that productive technology allows you to withdraw early without a positive return, although also without losses (one unit of the good is achieved at t=1). The problem is that the bank has promised a positive return (that is, interest) and if everyone withdraws their deposits, it means that there are more claims on goods than actual goods in the economy. In this case, the last depositors to withdraw their deposits are left with nothing. In this unstable equilibrium, it is precisely the transformation of liquid deposits into illiquid assets, what is usually called a term mismatch, that creates the possibility of bank panics.

In this scenario, the bank run equilibrium is an inefficient equilibrium since everyone has a deposit that pays on average 1, but might pay nothing if you come in last. The equilibrium is inefficient because simply by not using the banking system, a consumption of 1 could be achieved without any additional risk. Furthermore, it is an inefficient equilibrium because all productive activity with positive returns ceases. In the face of a banking panic, everyone withdraws deposits, and the bank liquidates its assets, preventing productive activity between t=1 and t=2 from taking place. Hence, everyone is worse off.

Wrapping up their explanation of the unstable equilibrium, the authors point out that the start of panics are usually produced by random events that cause concern in the economy, even if they have nothing to do with the solvency or safety of banks. They even claim that sunspots can cause a bank run. Of course, the latter is the subject of subsequent criticism, and it possibly led to the most criticism of this model. This prompted other researchers to make small changes to the model so that external shocks trigger the bank runs, very much in line with real business cycle theory that also became very fashionable in the 1980s, at the time of the Diamond-Dybvig paper. The key, in any case, is that any event can trigger a panic at t=1, because the bank’s situation is complicated at that period, as its assets have a lower net asset value than its deposit liabilities.

How to Solve Bank Runs in the Diamond-Dybvig Model?

Therefore, the Diamond-Dybvig banking model produces a possible efficient equilibrium where type 1 consumers and type 2 consumers are much better off, as well as a possible inefficient equilibrium where everyone is worse off, and the real economy is also affected by a drop in productive investment.

The next question both researchers ask is: how to avoid financial panics and achieve an efficient system?

Diamond and Dybvig begin by telling us that the traditional way for the banking system to deal with financial panics has been to decree a bank holiday (closing banks to avoid the withdrawal of deposits). In this way, it is avoided that some depositors will be left without any possibility of consuming, and time would be given for investments to mature. In our scheme, we would allow time for the productive process to reach t=2 and we would also avoid damage to the productive sector of the economy. The problem is that this solution can only be efficient if the banking sector is capable of differentiating between type 1 consumers and type 2 consumers. Since it is practically impossible for the bank to know who a type 1 consumer and a type 2 consumer is, then the only solution is to prevent everyone from withdrawing their deposits and consuming. This has the disadvantage of being inefficient for type 1 consumers, who wanted to consume at t=1 and are forced to do so at t=2 when their utility of consuming is equal to zero. Therefore, it is not a good alternative.

Thus, the authors argue, we must look for alternative solutions. And this is where politics and economics become one. Among all the possible options, according to the Nobel Prize winners Diamond and Dybvig, deposit insurance provided by government is the optimal solution. The idea is that governments can spend, by insuring bank deposits, supposedly efficiently produced tax revenues on those who withdraw their money at t=1. After trying to convince us by introducing into the equations the assumptions of tax-financed public insurance for depositors who withdraw their money at t=1, the authors tell us that even inefficient taxes are sufficient to generate an efficient equilibrium. The advantage of public deposit insurance is to prevent type 2 consumers from panicking, besides the credibility of government-backing as government can impose any type of tax, even inefficient taxes, means that type 2 consumers never withdraw their money from the bank. Therefore, a public deposit insurance would avoid an overliquidation of real assets, avoiding the losses of efficiency that we have mentioned before.

Therefore, the idea is that the public sector should establish deposit insurance, since it is better able to produce credibility than the private sector. With the assurance that deposits will be made whole, the possibility of bank runs disappears.

To finalize the model, and as if it were not enough, they argue that an alternative to government deposit insurance is using the central bank as a lender of last resort that purchases bank assets at a price above their current value at t=1, knowing that at t=2 the same assets will be much more valuable. Here the idea is that assets are prevented from being liquidated and very profitable productive activities are also avoided. In all fairness, it should be mentioned that the authors themselves comment that in the presence of more realistic schemes (such as the possibility of choosing between various types of productive assets instead of just one), the lender of last resort suffers from serious problems of moral hazard, problems that according to them are avoided in the case of government deposit insurance. Of course, none of this is actually taken into account in the model.

And well, this is basically the Diamond-Dybvig model. This model is the main reason why these two economists have won the Nobel Prize in economics. There are some other developments cited by the jury to award the Nobel Prize, but this model is undoubtedly the main one. In addition, the article explaining the model is one of the most cited monetary economics articles in history.

In a future article I am going to criticize the model I have just exposed and I will also expose the few really interesting points that do have application to the current financial world. I will end the next article with a possible explanation for why such a flawed piece of theoretical economics has achieved such fame as to be awarded the world’s top economics prize.

Legal disclaimer: the analysis contained in this article is the exclusive work of its author, the assertions made are not necessarily shared nor are they the official position of the Francisco Marroquín University.

—

[1] A small side note: that the productive technology produces two units of the good is a minor modification that we make for didactic reasons that does not alter the nature of the model.

[2] This feature of the model is almost reminiscent of the Hobbesian “state of nature” or taking autarky to its most extreme consequences.

[3] In the model scheme, R (productive payoff) is greater than the temporary discount ρ.

[4] The assumption of risk-averse consumers, despite being a simplification, is perhaps one of the most defensible of assumptions that we have reviewed so far.

Get our free exclusive report on our unique methodology to predict recessions

Daniel Fernández

Daniel Fernández is the founder of UFM Market Trends and professor of economics at the Francisco Marroquín University. He holds a PhD in Applied Economics at the Rey Juan Carlos University in Madrid and was also a fellow at the Mises Institute. He holds a master in Austrian Economics the Rey Juan Carlos University and a master in Applied Economics from the University of Alcalá in Madrid.

Get our free exclusive report on our unique methodology to predict recessions