The Gold Market vs Sovereign Debt

By Dickson Buchanan Jr.

The gold market, along with US and Chinese equities has shown a lot of volatility recently, causing many financial commentators to question its relevance for the today’s modern financial arena. It’s become quite common to underestimate gold’s importance in today’s sophisticated global capital markets. However, that perception tends to change when one actually takes a look at the data.

Gold is the only other asset, besides sovereign debt, which is held as a reserve asset on central bank’s balance sheets. The breadth, depth, and liquidity of the gold market are part of the reason why this is the case. To start, let’s consider the size of the global market for gold. The total above ground stock of physical gold is officially reported by the World Gold Council to be around 180,000 tons at the end of 2014. That’s around 5.7 billion ounces. At today’s dollar price of gold (around $1100) gold price, that’s about $6.3 Trillion dollars.

While this seems like a lot, the reality is that this figure could be a gross underestimation of the real supply because people have been accumulating gold long before anyone was trying to keep track of it.

Of course, only a percentage of that total stock of gold (180,000 tons) should be considered the financial market for gold. Jewelry still makes up a significant percentage of the total gold stock – close to 50%. However, that figure can be also be misleading considering that in many cultures such as China and India (the two largest consumers of gold), gold jewelry is often bought with the dual purpose of serving as an ornament and as a store of wealth.

Nevertheless, even discounting the market for Jewelry, the financial market for gold still ends up being gargantuan – reaching a market capitalization of $3 Trillion by conservative estimates.

Market Breadth:

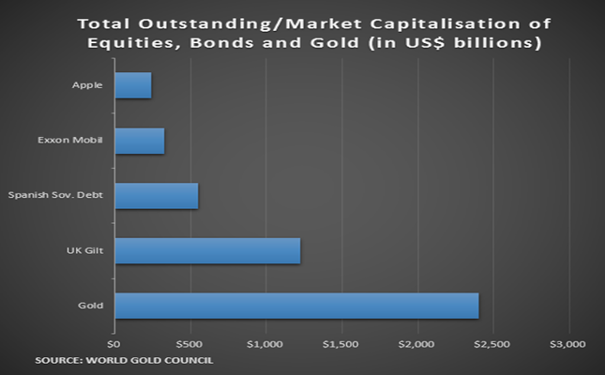

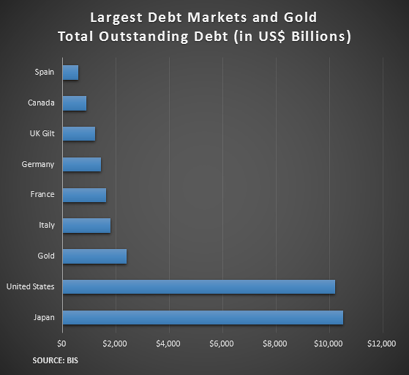

To put the size of the global market for gold into perspective, consider the following graphs provided by the World Gold Council.

Source: World Gold Council – Liquidity in the Gold Market

Source: BIS = Bank of International Settlements

The sheer size of the gold market makes it one of the most readily available and accessible financial assets in the world today. The World Gold Council has this to say,

“gold ranks higher than all European sovereign debt markets and trails only US Treasuries and Japanese government bonds. Thus, simply based on size…the gold market can provide significant depth and liquidity for large reserve portfolios, as it is only surpassed in size by two sovereign debt markets (US and Japan).” (pg. 6 Liquidity in the Gold market)

It follows then that gold is the third largest reserve asset held by central banks around the world behind only the dollar and euro denominated assets. The financial market for gold is so large the only other markets worth comparing it are sovereign debt markets. Given that sovereign debt is the asset which matches the liability of sovereign currencies, ultimately this places gold in the same financial category as currency.

Market depth and liquidity:

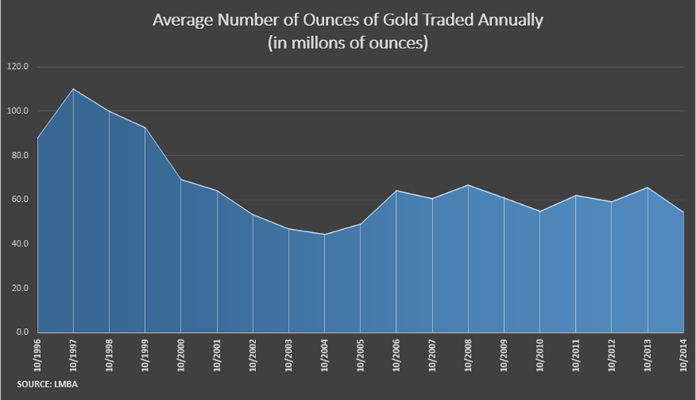

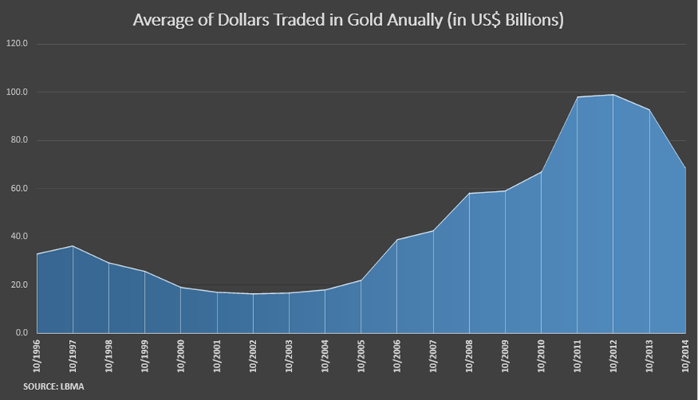

Additionally, the depth of the gold market and its liquidity are nearly unparalleled. Average trading volumes for gold are among the largest of any financial asset and in most cases are actually greater than most all major sovereign debt markets save only US treasuries. The following charts illustrate this reality.

Source: LBMA – London Bullion Market Association

Source: LBMA – London Bullion Market Association

While these figures are believed to be an accurate representation, they do not paint the entire picture as they represent only the movement of physical gold trades. Since, many trades between different bullion banks and firms are often netted against one another, it often underrepresents the true volume. To this point, the WGC reports,

“Many dealers estimate that actual daily turnover is an absolute minimum of three times the amount of transfers reported by the LBMA and could be upwards of ten times higher. This would put global OTC trading volumes anywhere between $67 and $224 billion. Using the more conservative estimate of $67 billion means that average daily trading volumes in gold are larger than the UK gilt market and the German bund market combined.”

In addition to exceptional market depth, the gold market is extraordinarily liquid, boasting some of the tightest bid-ask spreads. Average spreads in the global OTC gold market are anywhere from $.50 to $.85 per oz. Depending on the dollar price per ounce, that comes out to be around 0.04% to 0.07%. Once again, only the market for US treasuries can boast spreads as tight as gold.

Conclusion: Gold vs Sovereign Debt

As one can see from the aforementioned market data, the gold market is clearly one of the largest and most important financial markets in the world today. Despite what certain economists or politicians would have us believe, gold is neither barbarous, nor a relic. It is a highly sophisticated, evolved and active market. The breadth, depth and liquidity of the global gold market attest to this fact.

In fact, the above data implies that the only comparable markets to gold are sovereign debt markets. This is significant because essentially sovereign debt is a very different type of asset compared to gold. One market is subject to downgrades in quality, risk premiums, and ultimately default. The other is not as it carries no counterparty risk whatsoever.

As an asset class, gold remains one of the most liquid and robust financial assets in the modern financial frontier. Meanwhile, sovereign debt which is as liquid or more, has empirically proven to suffer huge catastrophic losses in capital and liquidity suddenly posing a systemic risk to the current system.

In today’s financial landscape, sovereign debt and the counterparty risk it poses to creditors is becoming an increasingly important issue that investors should be aware of. One only need look to Greece and the Eurozone as a fresh example in a long history of many others.

Dickson Buchanan Jr. is the Director of International Development and a Senior Precious Metals Broker at SchiffGold, as well as the Managing Director of SchiffOro. He holds an MA in Economics from King Juan Carlos University and regularly contributes commentary and analysis on gold, financial markets, and entrepreneurship. His interests include monetary theory, capital theory, entrepreneurship and the history of economic thought. You can contact him directly at dickson@schifforo.com

Get our free exclusive report on our unique methodology to predict recessions

Dickson Buchanan

Dickson Buchanan Jr. graduated in Business Administration and has a master´s degree in Austrian school economics.

He is currently working with Peter Schiff as Director of international development, issues research and analysis of the precious metals markets. He writes regularly on themes related to the importance of gold.

His research interests are monetary theory, theory of capital, entrepreneurship and history of economic thought.

Get our free exclusive report on our unique methodology to predict recessions