Mexico’s Central Bank Reacts to the Fed’s Rate Hike

By Edgar Ortiz December 28, 2015

Translated from Spanish by Katarina Hall

The most notable news in the economics and finance world has been the Federal Reserve’s decision to raise interest rates on December 16th. In response to the news, Mexico’s Central Bank raised its interest rate target by 0.25 percentage point.

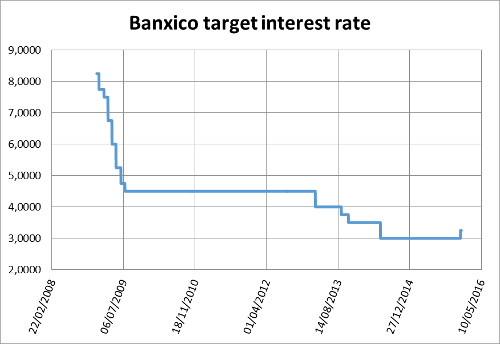

Since mid-2009, Banxico had maintained a policy of “easy money,” similar to the one held the Federal Reserve. As observed in the graph, the Bank of Mexico lowered the interest rates from 8.25% in January 2009 to 4.5% in July of the same year. By then, the Fed already held its rates near to zero.

Source: Bank of Mexico.

As we can see, on December 17th Banxico raised interest rates from 3% to 3.25%, only a day after the Fed did the same. Was Banxico’s move wise?

To begin with, there are many reasons to think that the Mexican economy is moving at its own pace, and the main indicators seem to point out that the Mexican economy is stable. Unemployment rate is at 4.2%, GDP is growing at a modest, yet stable, pace of 2.6%, among others other factors. These will be addressed in greater detail in our next trimestral report on the Mexican economy.

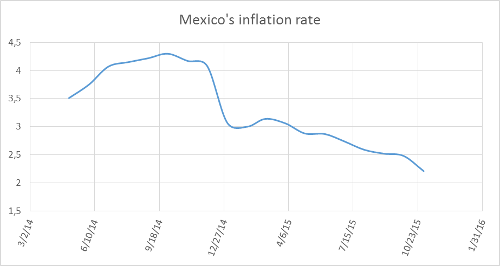

Secondly, what caused further discussion about whether or not to raise interest rates is the inflation target. Banxico targets inflation at 3%. Yet the currently inflation is around 2.2 or 2.3%. Even though the inflation numbers are below the goal, they are still acceptable.

Source: Bank of Mexico.

The last factor we should take into account is the exchange rate. In a previous article we already discussed the devaluation the Mexican peso suffered due to the drop in oil prices. In the article, we mentioned how the peso went from 13.20 to the dollar in January 2014 to the current 17.2 pesos to the dollar—a devaluation of 23.3%. We have to keep in mind that the peso was devalued more than 4% between November and December of this year.

Most likely this month’s currency devaluation can be explained, among other factors, by the forecast of the Fed’s decision. For now, it seems like Banxico’s decision was the correct one, at least in the short term. The United States is Mexico’s greatest commercial partner, which make the hits and misses of American monetary policy affect Mexico’s.

For now, the only thing the central bank can do is react. So far, the decision to avoid the peso’s further devaluation has proved wise, yet the recovery of the currency depend on factors of the real economy.

Get our free exclusive report on our unique methodology to predict recessions

Edgar Ortiz

Edgar Ortiz has a degree in Law from the Francisco Marroquín University. He holds a master in Austrian Economics at the Rey Juan Carlos University in Madrid. He is the executive director of the Center of Economic and Social Studies (CEES). He is a professor of economics at the Francisco Marroquín University, and he is also an analyst on issues related to the situation at Canal Antigua. He works as an associate lawyer at Estudio Jurídico Rivera.

Get our free exclusive report on our unique methodology to predict recessions